Treasury Stress

March 31, 2026

Everyone is watching crude. We are watching Treasuries.

The U.S. government is borrowing trillions of short-term debt. That worked fine when rates were below 1% (2012-2017, 2020-2021). Today, Treasury is rolling short-duration debt at higher rates, with the 3-month T-bill currently yielding around 3.7% (source: Bloomberg).

Before the Iran War, February’s Quarterly Refunding signaled shrinking deficits and strong demand. That backdrop reversed immediately when the Iran War started. Slower growth, surging defense spending, and a hawkish Fed pivot are forcing markets to absorb materially higher issuance.

Auctions are tailing. A tail is the bond market’s version of a stock offering that has to be repriced at a higher yield to get done. It signals either insufficient demand, too much supply, or both. According to Bloomberg, on March 24, a two-year note auction for $69 billion drew unexpectedly weak demand as investors worry a protracted war could spark an oil-driven inflationary resurgence, suggesting yields should be higher.

The compounding risk arrives in April. Tax season drains reserves from the banking system at precisely the moment the Fed’s $40 billion monthly balance sheet expansion slows. Hedge fund deleveraging in repo markets and tightening swap spreads confirm the stress is real.

The Hormuz headlines are loud. The Treasury market is quiet. In our experience, quiet warnings matter most.

Data as of 03/30/2026. Source: Bloomberg.

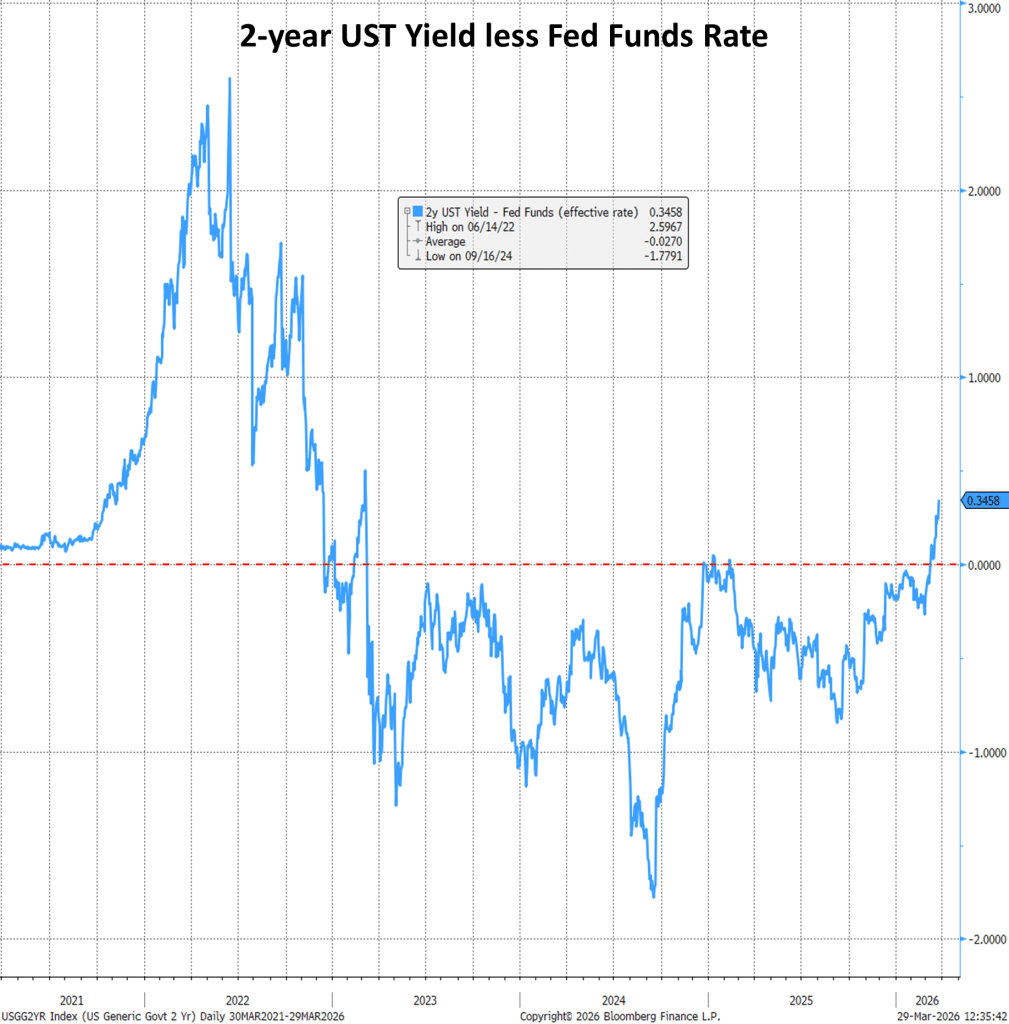

The line represents the spread between the 2-year US Treasury yield and the effective Fed Funds Rate. When the spread surges, the bond market signals that the Fed needs to raise rates.

Past performance does not guarantee future results. It is not possible to invest directly in an index. Index performance does not reflect the costs of managing a portfolio or the fees and expenses associated with investing in securities.